")

Fuel, fertilisers, and forex – the 3Fs that India is focusing on. But why? The US-Iran war has put the global economy at risk, and India is not immune. In fact, in the current context it is vulnerable due to its external dependencies for crude oil and fertilisers. A big portion of the population depends on agriculture for which fertilisers are an important input. Fuel – be it crude oil, LPG, or LNG – powers economic growth and day-to-day life.Finance Minister Nirmala Sitharaman recently urged the country to focus on fuel, fertiliser and foreign exchange and underlined that PM Narendra Modi’s appeal to conserve foreign exchange was “very important” amid the Middle East conflict.“The Prime Minister giving a call to conserve foreign exchange, as far as possible, is very important,” Sitharaman said. She said that the stress on 3Fs – fuel, fertiliser and foreign exchange – should be viewed in this context.So why are these 3Fs so important? How do they add to pressure on India’s growth story? We decode:

Fuel

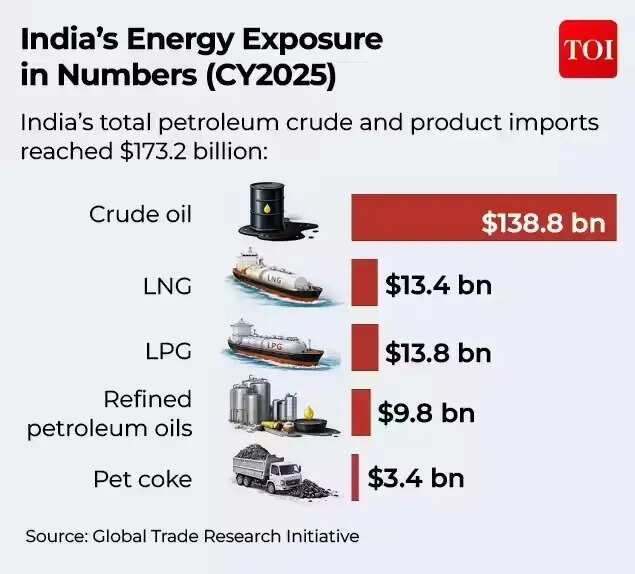

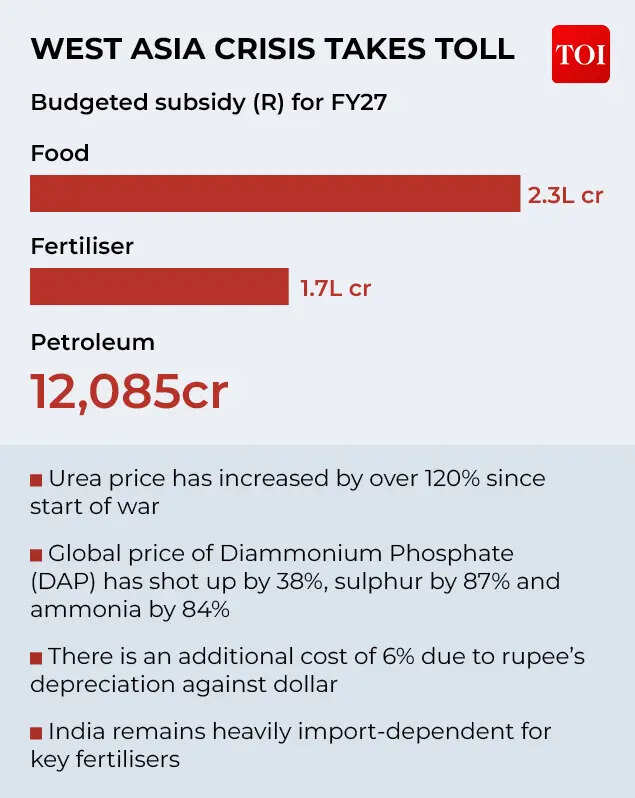

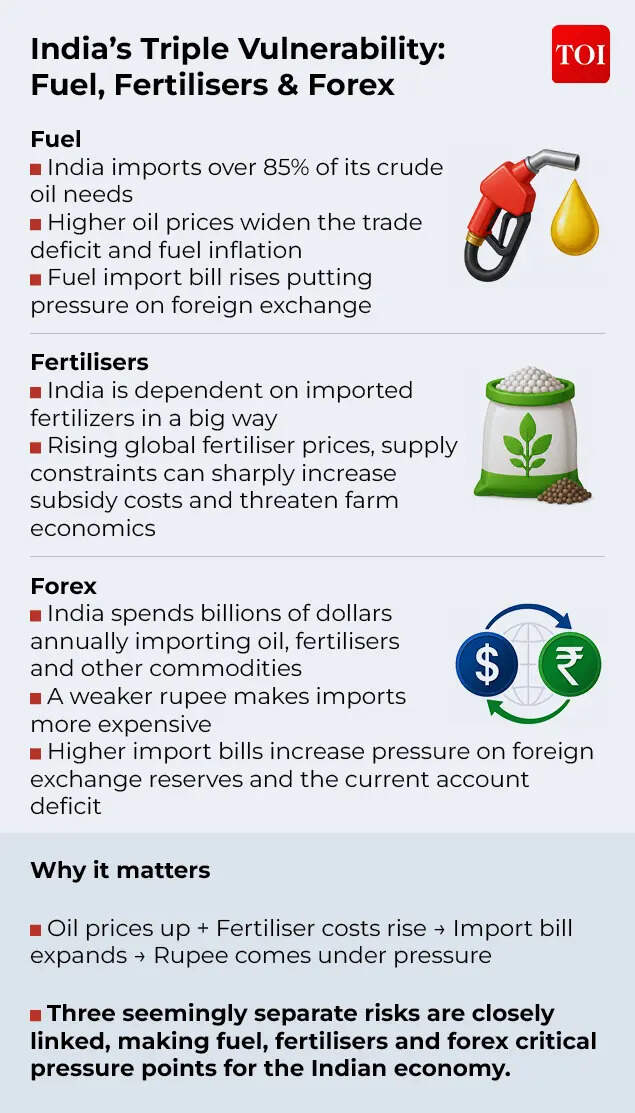

Your car, your kitchen, cabs, trucks for transportation, and industry – everything runs on fuel – be it petrol, diesel or LPG. And India imports most of its fuel needs – in fact in the case of crude oil the dependence is as high as over 85%! And a lot of that fuel comes from the Middle East countries. One of the first fallouts of the US-Iran conflict has been the skyrocketing global crude oil prices and major supply constraints for oil and gas due to closure of the Strait of Hormuz. The government has assured that there is adequate supply of crude oil and LPG, but the issue is not just about availability. It’s the higher cost of availability.You are already feeling the impact of it – petrol, diesel and CNG prices have risen. LPG – both domestic and commercial – has become more expensive. Pressure is also mounting on the cooking gas subsidy front. The Union Budget earmarked Rs 12,085 crore for LPG support this year, but that allocation may prove insufficient.The government had already compensated oil marketing companies with around Rs 26,000 crore for the previous year, while state-owned fuel retailers are currently estimated to be losing about Rs 700 on every domestic LPG cylinder sold. The quota for subsidised LPG cylinders has been reduced.Additionally, earlier cuts in excise duty on petrol and diesel have reduced government revenues by more than Rs 1 lakh crore annually.

From an economic standpoint, a rise in crude oil prices means the import bill goes up. Any pass through to consumers feeds into inflation, which in turn impacts growth.DK Srivastava, Chief Policy Advisor, EY India sees no early end to the issue. “Even when the crisis is resolved, supply and price normalization may take two to three quarters at a minimum. Thus, the whole of 2026-27 is likely to be affected by this crisis. India’s dependence on imported crude is close to 90% and therefore, crude oil supply and price disruptions constitute a major vulnerability for the Indian economy. Since available crude is to be imported at higher prices, there is a pressure on forex reserves,” he explains.

Fertilisers

Much like fuel is essential to keep your cars and kitchens running, fertilisers are the fuel that power the agricultural sector. India imports a big portion of its fertiliser needs, heavily dependent on fertilisers like DAP, potash and NPK. According to this TOI report, 40 million tonnes of urea that is consumed annually, around 8-10 million tonnes is imported. Imports also account for around 60% of domestic DAP demand, while potash requirements are met entirely through overseas purchases. So what’s the problem? The Middle East accounts for around 50% of India’s DAP and urea imports. Saudi Arabia is the largest DAP supplier and Oman is the biggest urea supplier. Liquified natural gas or LNG, an important component for fertilisers, is also imported from the Middle East.The supply constraints via Strait of Hormuz come right ahead of monsoon season, and with predictions of El Nino disrupting rain patterns, it’s a double whammy. And supply is just one side of the problem. The cost of urea and other fertilisers has shot up substantially since the start of the conflict. This implies a ballooning fertiliser subsidy bill, which will put a strain on the government’s finances and fiscal deficit target.According to the TOI report mentioned above, the government’s fertiliser subsidy bill could touch Rs 3.8 lakh crore – that’s more than double of what was budgeted for!Urea prices have surged by more than 120% since the outbreak of the war. Prices of key inputs have also risen sharply, with DAP increasing by 38%, sulphur by 87% and ammonia by 84%. A weaker rupee has added to the burden, increasing costs by another 6%.

DK Srivastava of EY India explains, “Considering Nitrogenous, Phosphatic and Potassic fertilisers together, India’s import dependence amounts to about 31%, which is the average over 2021-22 to 2024-25.” “In 2026-27, this vulnerability is particularly material because agricultural output is likely to come under pressure from a likely significantly below normal monsoon due to the expectation of a severe El Nino,” he tells TOI.

Forex

Foreign exchange reserves form the backbone of a country’s external sector. Anything a country imports requires forex outflow – which means that if the cost of imported items goes up, so does the forex outflow, hence reducing the reserves.India’s external sector resilience, with an import cover of around 11 months, has been hailed by experts. But, a falling rupee and higher import bills are putting pressure, and one that the government has been quick to point out. And, as DK Srivastava points out: the pressure on forex reserves is also arising from other factors particularly outflow of funds from India. Net portfolio investment was negative at $16.7 billion in 2025-26. Even the net FDI was negative through the months of August 2025 to January 2026 although there was some recovery in February and March 2026.PM Narendra Modi recently appealed to citizens to avoid buying gold. Why? Because India imports a huge amount of gold – and the government doesn’t see it as a necessary commodity that forex reserves should be spent on.The take is simple: the country has enough foreign exchange reserves, but it should choose to use them wisely for products of critical importance such as fuel and fertilisers. Higher foreign exchange reserves also allow the Reserve Bank of India to intervene and prevent the rupee from falling too much.“As on May 29, 2026, India’s foreign exchange reserves stood at a healthy $682.3 billion, adequate in terms of the standard metrics of reserve adequacy including import cover (about 11 months) and external debt (89.1 per cent). Various policy initiatives are expected to strengthen our balance of payments,” RBI governor Sanjay Malhotra recently said. But, forex reserves have fallen from their all time high, and the vulnerability associated with geopolitical uncertainties is causing the worry.

How the 3Fs tie up to be worry points:

Dependency on fuel and fertilisers feeds into need for higher forex outflow as the country pays higher due to rising global prices. This puts pressure on the foreign exchange reserves, with the potential to trigger a vicious cycle. DK Srivastava of EY India explains:High fuel prices in the presence of a depreciating rupee puts additional pressure on available foreign exchange reserves. The expectation that these reserves may be depleted further leads to further depreciation of the rupee making the rupee cost of imported fuel even higher. As the government tries to limit the passthrough to the users and consumers of petroleum products by absorbing some of the costs, government subsidies are likely to increase. Fertilisers are likely to cost more both because of supply bottlenecks and higher import prices.

Together these constitute a vicious cycle starting from higher crude prices, higher fertiliser prices, further depreciation of the rupee, higher inflation within the economy and lower growth. Lower growth and higher subsidies lead to higher current account and fiscal imbalances which puts additional pressure on the Indian rupee and depletion of forex reserves. The biggest immediate risk continues to be the fuel supply bottlenecks and higher than trend prices since its impact is spread throughout the economy affecting input, transport and storage costs.

Structural risks?

Economists and experts are divided on whether the ongoing situation poses structural issues to the economy. However, they warn that India continues to be exposed and vulnerable to geopolitical risks due to its high energy and fertiliser needs dependence. Vivek Kumar, Economist at QuantEco doesn’t see any structural risk as yet.“India has a rich policy experience of dealing with external crises, and the current one has spurred the policymakers into action. The government and the RBI have jointly been addressing the most imminent short-term risk, which is the pressure on BoP, by trying to curb the current account deficit as well as incentivize targeted foreign capital inflows,” he tells TOI.“The longer-term policy response from the government involves the ongoing emphasis on trade diversification, rationalization of customs duties and other trade barriers, forging of new-age FTAs, internationalization of rupee, etc,” he adds.However, DK Srivastava of EY India cautions that the world economic and trade order is undergoing a major structural change. There has been, in recent years, a reversal of the earlier emphasis on multilateral and free trade characterized by low tariffs and limited quantitative restrictions. There has been a major change towards restrictions on trade through higher tariffs and quantitative restrictions.“Under these circumstances, India should prepare for frequent disruptions in supplies of fuel and fertilisers and price shocks relating to commodities. India has to emphasise building strategic reserves in respect of selected commodities to minimize the adverse impact of these shocks,” Srivastava says.“It also needs to augment domestic capacity to produce crude oil and fertilisers. A detailed re-orientation of India’s growth strategy is needed in order to protect its long-term growth potential,” he adds.Ranen Banerjee of PwC India sees these as structural challenges. “India needs to address this through policy measures that include diversifying its energy mix as well as exploring enhanced production of fertilisers from coal gas,” he says.He notes that this would take some time and in the interim, the economy will continue to face these risks emerging from every geopolitical conflict.The government has eased taxation on bonds and the RBI has announced several measures to attract foreign capital and NRI deposits. Imports of gold and silver have been disincentivised by hiking excise duties. All these steps are aimed at enhancing foreign exchange reserves, reducing outflows and protecting the rupee.If they start yielding results, India would continue to be comfortably placed to handle the rising crude and fertiliser bills. Though as economists note – the ultimate steps are required on the long-term front: building strategic fuel reserves, and reducing dependency on fertiliser imports.