US-Iran war impact: How can India shock-proof itself against future oil, LPG, LNG supply disruptions?

")

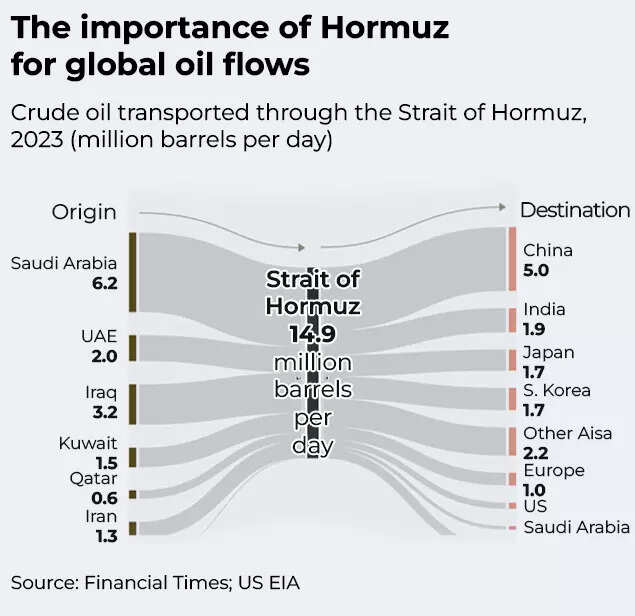

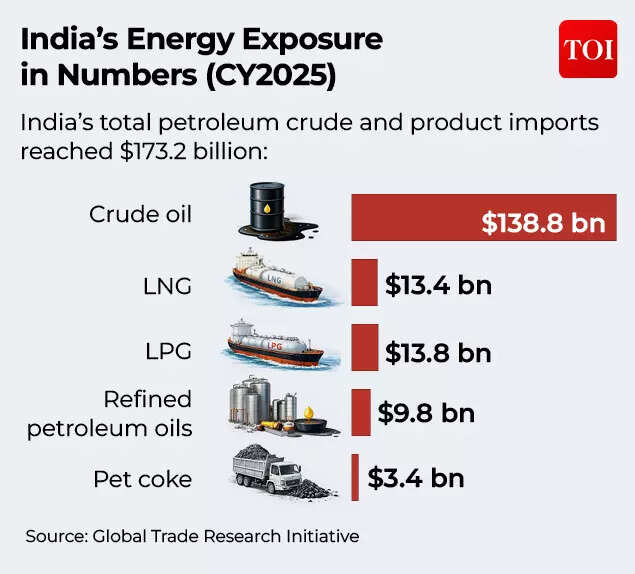

India imports around 90% of its crude oil needs, and approximately 60% and 50% of its LPG and LNG requirements respectively. These are not just mere statistics – it’s a telling picture of the energy needs and security needs of one of the world’s largest economies. This dependence has been put to test amidst the ongoing US-Iran war that has choked energy supply from one of the most important maritime routes – the Strait of Hormuz. The Middle East crisis has brought to fore with clarity an important fact – while India says it is comfortably placed on its oil, LPG, and LNG supplies – there is need to step up pace on long-term plans to ensure India’s energy security can cater to longer disruptions as well. India has built strategic petroleum reserves over the last few years and is better placed than before on its energy security, but the globally prescribed standard for reserves is 90 days, and India is below that.“West Asia remains a critical supplier for India’s energy needs. In 2025, about 48.7% of India’s crude oil imports, 68.4% of its LNG imports and more than 91% of its LPG imports came from the region. This high concentration exposes the Indian economy to sudden supply shocks,” notes Global Trade Research Initiative (GTRI) in its latest report.

What’s the current status of India’s energy security?

Experts note that while the domestic buffers for oil are relatively strong, LPG and LNG supplies need a boost. According to the government, India has 25 days of crude oil, its petrol and diesel can last another 25 days apart from the strategic oil reserves it maintains. Cooking gas stocks can last around 25-30 days, and liquefied natural gas stocks of around 10 days are available.India has the capacity to hold 5.33 million tonnes of crude in underground caverns at Visakhapatnam, Mangaluru and Padur – roughly 40 million barrels, or about 9–10 days of national demand. At present, around 80% of this is full. India has also stepped up purchases of Russian crude oil to tide over the immediate supply deficit.Sourav Mitra, Partner – Oil & Gas, Grant Thornton Bharat believes that India has quietly built depth into its energy security. Price volatility may be unavoidable – but the era of sudden physical shortages is steadily receding.

During the current bout of regional uncertainty, cargo-tracking data suggest that nearly 100 million barrels of commercial crude, including shipments already en route, are readily accessible – enough to cushion imports for another 40–45 days if Hormuz flows are disrupted. The immediate threat, in short, is not scarcity but cost, says Mitra.LPG supplies are also on firmer footing. India now has two underground storage ‘anchors’ on opposite coasts – at Visakhapatnam and Mangaluru – providing about 140,000 tonnes of deep storage. According to Mitra, natural gas remains the weak spot. “While India has eight LNG import terminals, it lacks a formal gas strategic reserve. Policymakers are now considering a practical workaround: earmarking a small, government-callable buffer within existing LNG tanks to manage supply or price shocks,” he says.

Which new strategic reserves projects are in the pipeline?

Oil (Strategic Petroleum Phase-II): As of the latest Parliamentary review, land at Chandikhol and Padur-II was yet to be handed over by state governments, even as FY26 funding lines have been opened, so commissioning looks staggered later in the decade rather than immediate. When operational, India’s strategic petroleum reserves (SPR) capacity rises from 5.33 MMT to 11.83 MMT, taking SPR-only cover from around 9–10 days towards 20 days, depending on demand, says Sourav Mitra of Grant Thornton Bharat.LPG: The HPCL Mangalore cavern was commissioned in September 2025. This has lifted underground LPG capacity to approximately 140,000 MT (Mangalore around 80,000 MT + Visakhapatnam 60,000 MT). In practice, national ‘days of cover’ for LPG depend on above-ground tanks and import cadence, but the two caverns now provide east–west strategic anchors. LNG: The 10% terminal-level strategic buffer is at draft stage; once notified, operators would phase in additional tankage or designate buffer volumes with government call-off protocols and cost-recovery. The recent chain of force majeure notices (QatarEnergy) has sharpened the case for quick notification, as a fast, low-capex way to add a national LNG backstop.

Insulating against future shocks: What should India do?

Experts stress the need for a multi-pronged strategy to deal with any future supply shocks. Apart from diversified procurement sources, domestic reserves need to be shored up to prevent both short-term and long-term supply shocks.Gaurav Moda of EY-Parthenon India says that the next phase of strategic petroleum reserves should be prioritised. “India can benefit further from acceleration of strategic expansion for Phase II that shall raise the strategic petroleum reserves to 11.83 MMT (which is an additional 17 – 18 days buffer); a separate feasibility study for six new strategic petroleum reserve locations is also underway for the next set,” he says.

Sourav Mitra of Grant Thornton Bharat advocates a gentle but important shift – from an LNG ‘strategy’ to an LNG ‘architecture’. The recent Qatar–Hormuz shock reminded us that contracts and terminals are necessary, but real resilience comes from owning, moving and trading molecules as well, he says, advocating the following:

- Broaden supply beyond a single anchor: India has prudently extended its long-term Qatar arrangement (7.5–8.5 mtpa through Petronet) and diversified with US volumes via GAIL; even so, at the national level, concentration remains meaningful. Adding term volumes from non-Hormuz geographies (US, Australia, West Africa) so that no single source exceeds ~30–35% would be a steady next step, he says.

- Pursue equity in producing assets: China’s NOCs hold stakes in 20% in Yamal, 20% in Arctic LNG 2, 5% in Qatar NFE, 25% in Australia’s APLNG-positions that provide flexibility in tight markets. Similar minority stakes in producing assets outside Hormuz can quietly improve India’s hand over time.

- Strengthen the trading and shipping spine: GAIL’s US FOB contracts and regular swap tenders are encouraging. Scaling a trading desk (JKM/TTF/Henry Hub hedging) and building a time-chartered LNG carrier pool would help India manage arbitrage and schedules during dislocations.

- Notify the 10% LNG buffer rule and drill the protocol: Turning the draft into a notified mechanism with clear call-off, replenishment and cost-recovery rules. This will offer a quick, affordable “gas SPR” across all terminals.

- Finish SPR-II and map SPR-III: Completing Chandikhol/ Padur-II and planning a third tranche would raise government-held crude coverage closer to IEA-style 90-day norms (alongside OMC stocks) as demand grows.

- Deepen LPG resilience: With Mangalore and Visakhapatnam caverns in place, a third site and VLGC jetty upgrades can gently lift household-fuel security.

- Keep crisis playbooks ready: The current LNG squeeze saw tactical curtailments to industry and protection for priority users. Codifying a National Fuel Substitution Protocol (for temporary LPG/naphtha/FO switches) and prudent price-risk hedging at PSUs can smooth the response in future events.

GTRI founder Ajay Srivastava is of the view that India should enter into long-term crude oil supply contracts with Russia. “Had India continued importing Russian oil at earlier levels – when it made up 35% of our crude imports – today’s energy concerns would likely be far less severe. India’s alternative supply options remain limited,” he says. Although imports from the United States rose 82% to $9.8 billion in 2025, the US itself runs a net crude deficit and has limited spare export capacity. “West African and Latin American crude supplies involve higher freight costs and longer shipping times. Long-term contracts with Russia would provide India with stable volumes, predictable pricing and a stronger buffer against global market volatility,” he says.Gaurav Moda recommends that for LNG, India may benefit from institutionalizing proposals to build 10% additional LNG storage capacity mandate for terminals and additionally facilitate financing for 3-4 bcm underground gas storage reserves that could be led by a combination of GAIL, ONGC and OIL. On the LPG front, India may benefit from policy initiatives to develop underground LPG strategic reserves, with a special focus on North and North-East, he says.“Countries like Japan and China have taken a larger view on such buffers to typically average 6 months plus in comparison,” he tells TOI.“In the long term, India may further strengthen and diversify its growth agenda through energy security via a three‑pronged strategic reserves framework similar to Japan, with a combination of national reserves, private storage mandates and joint stockpiling abroad at source,” he concludes.